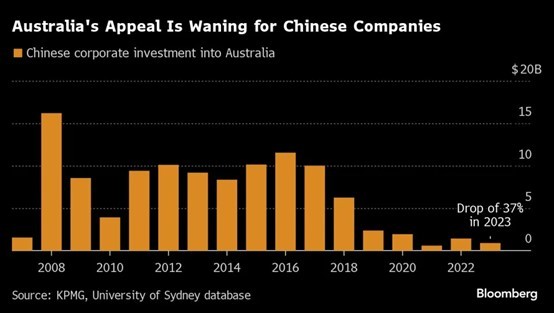

A report by KPMG and the University of Sydney revealed a significant drop in Chinese investment in Australia during 2023. Compared to 2022, the investment amount fell by 37%, going from US$1.42 billion to US$892 million. This decline is also reflected in Australian dollar terms, with a 36% decrease from AU$2.10 billion in 2022 to AU$1.34 billion in 2023. Direct investment from China fell by 37% marking the second-lowest level in 18 years. This decline comes in contrast to a global rise in China’s outbound investments, fueled by projects in countries involved in President Xi Jinping’s Belt and Road Initiative. The report, authored by Doug Ferguson (KPMG’s head of Asia & International Markets) and Helen Zhi Dent (KPMG’s China Business Practice partner), also highlighted a decrease in Chinese investment for traditionally attractive sectors in Australia, such as commercial real estate and mining.

The report suggests China might be shifting its Belt and Road Initiative (BRI) focus from building infrastructure and simply extracting resources in participating countries, towards establishing processing facilities. This could create “competitive challenges” for Australia, according to the report’s authors. China’s large investments in Indonesia’s nickel industry serve as an example of a potential threat. This influx of billions of dollars helped Indonesia transform into a major global supplier of nickel. Chinese companies provided the technology and funding needed for Indonesia to process its raw nickel into a higher-grade product, something Australia previously dominated. Indonesia’s newfound ability to produce this higher-grade nickel flooded the market, driving down prices and hurting Australian miners. This price drop forced Australian producers to cut jobs and production.

China’s economy is facing challenges. A struggling property market and weak consumer confidence are casting a shadow over its future growth. The report also highlights a significant decrease in Chinese investment abroad. Investment in the US has dropped to its lowest level in almost two decades, and investment in Australia has been declining for several years. This decline in Australia is partly due to rising political tensions between the two countries, which escalated under the previous Australian government. Trade sanctions imposed by China hurt Australian exports, though some have recently been lifted.

Chinese investment in Australia had been steadily declining even before the recent tensions. A 2021 report from the Australian National University illustrates this trend, showing a staggering 61% drop in Chinese investment in 2020, plummeting to $1 billion from $2.6 billion in 2019. This decline continued with a 47% decrease in 2019. These figures align with strained relations between the two countries, exacerbated by Australia’s call for stricter World Health Organization inspections in 2020, leading to threats of a Chinese consumer boycott. The 2022 demystifying Chinese investment report further confirms this trend, reporting a 70% decline in 2021 compared to the previous year, the lowest since 2007. Experts attribute this decline to a combination of factors, including inward shifts in China’s economic focus, tightened approval processes in Australia, and pandemic-related travel restrictions. This decline is not unique to Australia but part of a global trend as China prioritizes investments in Belt and Road Initiative countries.

The recent decline in Chinese investment in Australia can be attributed to stricter regulations placed by the Australian government on foreign investment in key sectors. These restrictions target areas considered sensitive, such as infrastructure and resources crucial for new technologies, like critical minerals. These minerals, including nickel, lithium and cobalt, are essential for developing clean energy sources, advanced manufacturing, and defense technology.

At the same time, there has been a dramatic rise in Japanese investments in Australia. A new report by Herbert Smith Freehills and Australian National University reveals a record year for Japanese investment in Australia in 2023. The total value reached A$133.8 billion, making Japan the second-largest trading partner and export destination for Australia. This strong relationship is driven by economic and political stability in Australia, along with a growing market and supportive government policies. The report dives into the details, highlighting a record 53 Japanese M&A deals in Australia, including big acquisitions like Kirin buying vitamins maker Blackmores. There’s also a trend of Japanese companies acquiring Australian startups to access new technologies. Interestingly, the focus is shifting towards sectors like real estate, consumer goods, and mining, alongside the ongoing importance of energy and resources. Looking ahead, the report predicts continued growth in 2024 due to favorable economic conditions. There’s also a focus on partnerships, with over 38 announced in 2023, especially in research and development between Australian universities and Japanese corporations. This collaboration is bringing together Australian research with Japanese capital and expertise, creating a promising future for the Japan-Australia relationship.

There is reason to conjecture meanwhile that Chinese FDI has changed direction. An August 2023 report by the Rhodium Group examines how China’s global outbound investment has changed since 2017. Overall, investment has slowed and shifted focus from developed economies to Southeast Asia. Chinese firms are also investing in new sectors beyond traditional ones, like advanced manufacturing and green technologies. The report analyzes these trends through case studies in Cambodia and Indonesia, highlighting both positive developments like increasing attention to sustainability and areas for improvement such as transparency and environmental impact.

The United States, Australia and the United Kingdom are the top three recipients of China’s outward foreign direct investment (FDI) since 2005, with the US in the lead at 197 billion USD. These developed economies were major destinations for China’s outward FDI. Australia was the second, with $130 billion.

China’s investments are likely to move away from developed countries due to increased scrutiny and flow more towards developing nations in Africa, South America, and the Middle East. This shift has already begun, with less decline in investments seen in those regions. A big driver for investment in developing countries is China’s Belt and Road Initiative (BRI) which focuses on construction projects. However, there are signs BRI might move beyond traditional building and invest in more advanced technological areas.

In 2022, Chinese mergers and acquisitions (M&A) of foreign companies plummeted to their lowest level since 2006, a more drastic decline compared to the global M&A decrease. This drop stemmed from various factors: stringent government regulations and capital controls curbed financing for overseas acquisitions, heightened international scrutiny deterred deals in sensitive sectors, and some Chinese firms self-censored to evade lengthy approval processes. This decline impacted major global markets, hinting at a challenging recovery amid ongoing geopolitical tensions and regulatory hurdles. As China reopens its economy, future M&A focus might shift towards Europe, Asia, and the Middle East, signaling potential changes in global investment patterns.

China’s prominent role in global foreign investment, historically centered on energy, metals, transport, and real estate sectors, is now witnessing a reversal. Developed nations’ increasing apprehension regarding Chinese investments in critical sectors, coupled with China’s own market access restrictions, suggests an impending decline in Chinese foreign investment and a shift towards economic segmentation. This shift complicates China’s aspirations for global leadership. The stark decline in trade with Australia vividly illustrates these evolving global economic dynamics. Reports from KPMG and the University of Sydney underscore this shift, highlighting a recalibration in economic strategies and regulatory scrutiny, particularly evident in sectors like commercial real estate and mining. These challenges highlight China’s struggle to maintain global economic influence amid geopolitical shifts and evolving trade dynamics.

*Dr Maheep is a leading analyst of International Relations and Global Politics, with a keen interest in Global Political Economy. He contributes articles on trending issues in these fields.

Leave a Reply